Use Desktop for Better Experience

Integrated Equity × Credit × Transaction Banking Report: Guangdong Investment 粵海投資 (HK0270)

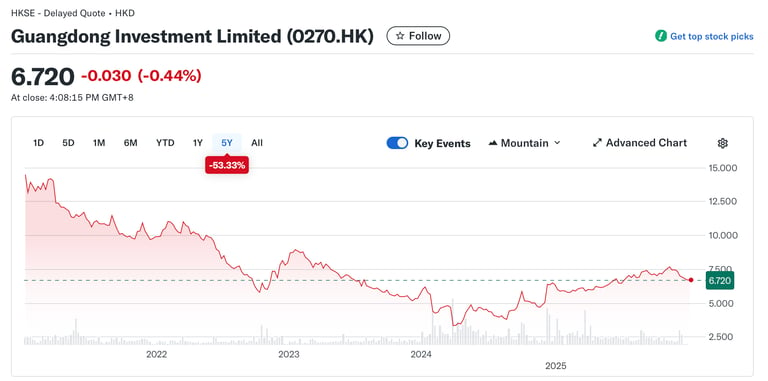

Price reference date: December 30, 2025 (close: HK$6.72). Latest audited annual filing referenced: Annual Report 2024 for the year ended December 31, 2024, released on HKEX on April 28, 2025.

FINANCIALSELECTED

Ryan Cheng

12/31/202517 min read

BUY

Investment Recommendation

*Stocks and investments carry risks, including the loss of principal. The views expressed on this blog are solely the opinions of the author at the time of writing and are subject to change at any time without notice.

*

Company Overview

-Company Background-

Guangdong Investment Limited (0270.HK) is a Hong Kong–listed “red chip” investment holding company whose controlling shareholder is Guangdong Holdings Limited (via GDH Limited, holding about 58.26%). The company traces back to Union Globe Development Limited, incorporated and listed in Hong Kong in 1973; a Guangdong provincial government–owned enterprise became the majority shareholder in 1987, and the company was renamed Guangdong Investment Limited in 1988. Today, it is positioned as a Greater Bay Area–centric operator/investor, and is commonly viewed as defensive because a large portion of its earnings and cash flow is anchored by regulated/contracted utility-style operations (especially its “Dongjiang water” franchise), complemented by commercial property, retail department stores, hotel ownership/management, and infrastructure/energy assets.

-Products-

(raw water supply, water distribution, wastewater) The group’s flagship asset is the Dongshen Water Supply Project, in which it holds an effective interest of about 95.08%. This project supplies unprocessed natural water (often described as “Dongjiang water”) to Hong Kong, Shenzhen, and Dongguan under a 30‑year concession commencing 18 August 2000, covering operation/maintenance as well as development and upgrades. The project has operated since March 1965 and is described as a large-scale transfer system transporting water roughly 69 km; after major renovation works (completed 2003), its designed annual supply capacity is about 2.423 billion tons. Importantly, the “Dongjiang water” source is the Dongjiang River (東江 / East River), a key Pearl River tributary: Hong Kong’s Water Supplies Department describes Dongjiang raw water as extracted from Taiyuan Pumping Station in Dongguan, conveyed via dedicated aqueduct infrastructure and discharged into the Shenzhen Reservoir before being pumped across the boundary to Hong Kong’s Muk Wu Raw Water Pumping Station (then distributed through Hong Kong’s major raw-water routes/reservoirs). Beyond Dongshen, Guangdong Investment also operates/invests in “Other Water Resources Projects” across Mainland China, including tap water supply, sewage treatment operations, and waterworks construction, with substantial designed daily water-supply and wastewater-treatment capacities disclosed at group level.

Water Resources

Property Investment & Development

(commercial/office and mixed-use assets) In property, Guangdong Investment’s platform is largely built around the GDH Teem group, where it holds effective interests of about 76.13% in Guangdong Teem (Holdings) and 76.02% in the Tianjin Teem entity (figures stated as of 31 Dec 2023). Through GDH Teem, it operates and/or holds major shopping-mall and commercial assets including Teem Plaza (Guangzhou) as well as Panyu Teemmall, Guangzhou Comic City, Shenzhen Teemmall, Yuehai Tiandi (粵海天地), and Tianjin Teemmall. The group also discloses ownership interests tied to Tianjin YueHai Teem Shopping Mall (a large mall in Tianjin’s “Binjiang Dao – Heping Road” commercial district, with significant floor area held for rental), and Panyu GDH Plaza—a large integrated commercial project in the Panyu Wanbo Central Business Districtthat includes (i) components held for sale (commercial residential units/offices) and (ii) a sizable mall complex branded as Panyu Teemall with substantial leasable commercial area.

Department Stores

(named stores / operators) The department-store business is run through specific operating companies and named stores, not just a generic “retail” description. Guangdong Investment states it holds an effective interest of about 85.2% in GDH Teem Commercial Co., Ltd. (GDTDS) and Guangzhou Teemall Department Store (廣州市粤海天河城百貨商業有限公司). Under these entities, it operates: Teemall Store (in Teem Plaza), Ao Ti Store (奧體歐萊斯名牌折扣店), Dong Pu Store (東圃百貨店), Hua Du Store (花都店), and Wan Bo Store (天河城百貨歐萊斯折扣店)—with the group disclosing total leased area across these stores. Separately, it also discloses an investment interest in Guangdong Aeon Teem Co., Ltd., described as a joint investment involving a group subsidiary and a Japanese company (reflecting a JV structure rather than wholly controlled operations).

Hotels

(owned hotels + what the hotel management team manages) Guangdong Investment’s hotel exposure includes both owned hotels and a broader hotel management business. As of 31 Dec 2023, it states its hotel management team managed 20 hotels (3 in Hong Kong and 17 in Mainland China) and that the group owned six hotels (two each in Hong Kong and Zhuhai, plus one each in Shenzhen and Guangzhou). The company lists named properties including The Wharney Hotel (Hong Kong), Oasis Avenue – A GDH Hotel (Hong Kong), Guangdong Hotel (Shen Zhen), and Guangdong Hotel (Zhu Hai). It also clarifies an important nuance for readers: among the owned hotels, Holiday Inn Zhuhai City Center was operated under a franchise arrangement, and Sheraton Guangzhou Hotel was managed by another hotel management group (i.e., not by the group’s own hotel management team).

Infrastructure & Energy

In infrastructure, Guangdong Investment discloses specific, named assets across energy and transport/municipal roads. On the energy side, it holds an effective interest of 71.25% in GDH Energy (中山粤海能源有限公司), which has twopower generation units totaling 600 MW installed capacity, and an effective interest of 25% in Guangdong Yudean Jinghai Power Generation Co., Ltd., which has four units totaling 3,200 MW installed capacity. On the roads side, it wholly owns the operator of the Xingliu Expressway (a toll road in Guangxi forming part of the G80 Guangzhou–Kunming Expressway corridor), with a main line of about 100 km plus connection lines totaling about 53 km; it commenced operation in August 2003 with five toll stations and two service zones. In addition, the group discloses a Yinping PPP Project in Dongguan (Yinping Innovation Zone), covering the development of certain A‑grade highways, connecting roads, and municipal roads (non‑toll) plus ancillary services such as drainage, greening, and lighting, with disclosed development cost caps (in RMB) and ongoing project management/maintenance responsibilities.

Industry Analysis

-Market Overview-

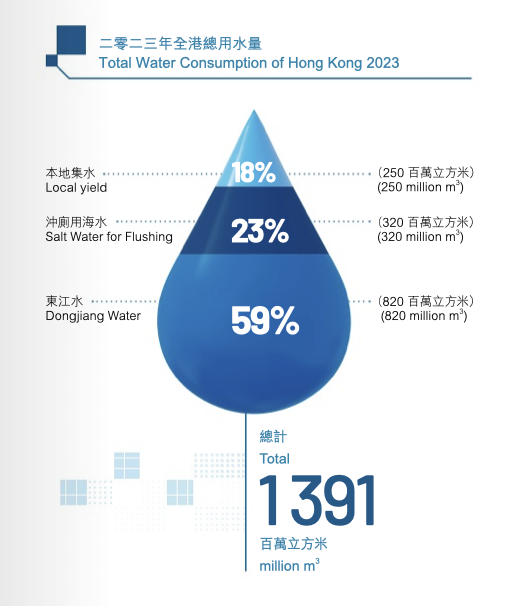

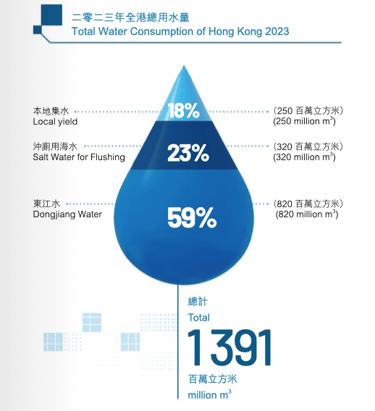

Guangdong Investment (0270.HK) is best understood through the lens of Hong Kong’s potable-water supply system and the cross‑border “Dongjiang (East River) water” import arrangement. Hong Kong’s water security is built around three sources: (1) local yield from rainfall captured in reservoirs, (2) imported Dongjiang water from Guangdong, and (3) seawater for toilet flushing (a separate non‑potable network). In 2023, the Water Supplies Department (WSD) reported total water consumption of about 1,391 million m³, split roughly into 18% local yield (250 million m³), 59% Dongjiang water (820 million m³), and 23% seawater for flushing (320 million m³).

That structure explains why the “industry” for 0270’s flagship water business is not a normal competitive market: imported Dongjiang water is procured and governed by government‑to‑government agreements (Hong Kong SAR ↔ Guangdong Province), using a package-deal framework with an annual supply ceiling and price mechanism. WSD notes that a new 3‑year Dongjiang water supply agreement for 2024–2026 was signed in December 2023, continuing the “package deal deductible sum” approach and indicating that the framework will be maintained at least up to 2029; WSD also discloses Hong Kong’s expenditure on Dongjiang water (e.g., HK$5,016 million in 2023).

The market is effectively policy + contract driven, where competitive substitution is limited in the short run because water security is treated as critical infrastructure, not a typical tendered commodity.

-Growth Forecasts-

For the Hong Kong potable-water market, the key driver is not “rapid demand growth” but system resilience under climate uncertainty and demand management. In WSD’s Total Water Management Strategy (2019 update), the government states it has updated demand/supply projections up to 2040 and anticipates annual fresh water consumption will be maintained around the current level with continued demand-management initiatives; it also concludes the current supply arrangement should meet forecast demand to 2040 with enhanced resilience. Water volume growth to Hong Kong is not the base case (it’s more like “stable baseline volumes”). Revenue growth (to the extent it occurs) is more likely to be price-mechanism/inflation/FX adjustments and contract renewals, rather than ever-increasing water sales volume.

Desalination exists, but (today) it’s positioned as diversification/back-up, not a full replacement. Hong Kong is investing in desalination primarily to diversify and improve resilience, not to “replace” Dongjiang water quickly. WSD’s published strategy materials describe the Tseung Kwan O desalination plant as a supply-management initiative under Total Water Management, with 135,000 m³/day capacity and provision to expand to 270,000 m³/day, targeting roughly ~5% and potentially ~10% of Hong Kong’s overall fresh-water demand.

Because the arrangement is governed by agreements, the “growth forecast” for the Dongjiang-water segment is best described as: High visibility / stability as long as agreements continue; and

Incremental revenue uplift tied to the agreement’s pricing adjustments rather than competitive dynamics. WSD explicitly notes that under the 2024–2026 agreement, the annual ceiling water prices increase by 2.39% each year, reflecting relevant CPIs and RMB/HKD exchange-rate movements.

Outside the Hong Kong import-water niche, Guangdong Investment also participates in mainland water supply / wastewater treatment-related operations. That part of the industry tends to be driven by: environmental compliance (tighter discharge standards), municipal investment cycles, industrial wastewater needs, and technology upgrades.

Industry research providers estimate mid‑single‑digit to high‑single‑digit growth rates in various China water/wastewater sub-segments through 2030 (the exact numbers vary by definition). For example, Grand View Research’s “horizon” pages show: China primary water & wastewater treatment equipment: ~5.8% CAGR (2025–2030) . China biological wastewater treatment: ~7.5% CAGR (2025–2030).

This “other projects” water/wastewater exposure can offer growth optionality, but it’s generally less monopoly-like than the Hong Kong Dongjiang supply framework, and may be more sensitive to capex cycles, regulation, and competition.

-Catalysts for Market Growth-

Contract Continuity + Price Mechanics

Greater Bay Area Urbanisation & Industrial Upgrading

Concession-style Economics of Core Water Asset

For the flagship Dongshen/Dongjiang water business, the most important growth catalyst is contract renewal/continuity and the pricing mechanism under the government-to-government supply arrangement. Hong Kong signed a new 2024–2026 Dongjiang water supply agreement that continues the “package deal deductible sum” approach and includes an annual ceiling price increase (reported as 2.39% per year) tied to indices and RMB/HKD FX considerations. Even if volumes are stable, revenue can still trend upward if the agreement’s ceiling price or indexation steps up.

Outside Hong Kong supply, Guangdong Investment also operates/invests in mainland water distribution and wastewater/sewage treatment projects. In many Chinese cities, water/wastewater demand and standards are driven by: urban population concentration, industrial transformation (higher-quality discharge standards), “pipe network” upgrades and leakage reduction, municipal PPP/project pipelines. This area is typically more competitive and tender-driven than Hong Kong import water, but it can offer higher growth when municipal capex cycles are favorable (and when the company’s financing/PPP execution is strong).

Guangdong Investment states the Dongshen Water Supply Project is a core business, with an effective interest ~95.08%, supplying natural water to Hong Kong, Shenzhen, and Dongguan, under a 30-year concession commencing 18 August 2000. A “utility-style” asset base can be a catalyst for: lower earnings volatility, access to longer-tenor financing, steady dividend capacity, and potentially more stable valuation vs cyclical property/retail.

-Porter's 5 Forces Analysis-

Core water (Hong Kong/Shenzhen/Dongguan raw water supply): Rivalry is low because the business behaves less like a free market and more like a strategic, agreement-based supply framework; Guangdong Investment’s Dongshen project is positioned as the long-running infrastructure operator supplying these regions.

Mainland water/wastewater projects: rivalry is higher—tenders/PPPs often attract multiple operators (state-owned and private environmental firms). Property, department stores, hotels: rivalry is typically high (many substitutes, cyclical demand, intense competition).

Competitive Rivalry

Core water: new entry is extremely difficult due to: capital intensity (large-scale water transfer infrastructure), regulatory and cross-border governance complexity, long asset lives and established operating arrangements. Desalination can be seen as an alternative supply project commissioned by the government.

Non-core businesses: property and hospitality have high entry barriers in prime locations (land scarcity), but competition still exists; retail has lower structural barriers.

Threat of New Entrants

For the flagship supply to Hong Kong, the “buyer” is effectively government-linked procurement (public-sector counterparty). That typically means: large, sophisticated buyer with negotiating leverage on contract structure, pricing approach, and volumes/ceilings, but also a buyer whose priority is security of supply, not just lowest price. So buyer power is high in negotiation terms, yet the relationship is also “sticky” because water security is not easily contestable.

In property/retail/hotels, buyer power can be meaningful (tenants and consumers have many choices), especially in downturns.

Buyer Power

Suppliers differ by segment: Core water: the input is water sourced via the regional system; the biggest supplier-type risks are: upstream hydrology and climate variability, energy costs for pumping/treatment, and maintenance/engineering services. Engineering & construction / equipment: supplier power can rise during capex booms (specialized contractors, materials), but generally it’s not monopolized. Energy/fuel and financing: for infrastructure-heavy utilities, financing conditions and interest rates can act like supplier power (cost of capital), especially when projects require ongoing upgrades.

Overall, supplier power is usually not the dominant force versus policy/contract dynamics.

Supplier Power

For Hong Kong potable water, substitutes are limited in the short term because imported Dongjiang water is a major component of the system. However, substitution at the margin is increasing due to: desalination (Tseung Kwan O plant: 135,000 m³/day, expandable to ~270,000 m³/day); demand management/leakage control (reduce total demand rather than replace supply); potential future reuse/reclaimed water options (policy-dependent).

This means the substitute threat is not “someone else takes Guangdong Investment’s customers tomorrow,” but rather: Hong Kong’s supply mix can diversify over time, limiting long-run volume upside from imported water.

Threat of Substitution

Investment Catalysts

-Hard Catalysts-

Dongjiang Water-supply Agreement Rollovers & Pricing Mechanism

For 0270, the single most important hard catalyst is the continuity and terms of the Hong Kong–Guangdong Dongjiang water supply agreement. In December 2023, Hong Kong announced a new 2024–2026 agreement that keeps the “package deal deductible sum” approach and specifies 2.39% annual increases in the annual ceiling water price (linked to Guangdong/HK price indices and RMB/HKD FX).

Even if water volumes are stable, this arrangement can provide visible revenue progression through the contractual pricing mechanism. Government materials also state the deductible-sum approach should be maintained at least up to 2029, reinforcing medium-term framework continuity.

Capex/Expansion Pipeline in “Other Water Resources Projects” (mainland)

Beyond the Hong Kong import-water franchise, GDI discloses ongoing investments in water supply plants and sewage treatment plants in Mainland China, including new construction/expansion projects and stated capacity numbers and expected investment amounts (e.g., projects and capacity figures disclosed “as at 31 December 2023”).

These projects can be incremental growth drivers that are less “policy-binary” than the HK supply agreement (but are typically more execution- and tender-driven). They can also change the consolidated growth profile if capex converts into allowed returns / operating profit.

Property/Retail/Hotel Cycle Turning Points

0270 is not “pure water.” Non-water segments are inherently more cyclical: Property rents/occupancy and asset valuation changes, department store footfall/consumption cycles, hotel RevPAR/occupancy cycles (and tourism/business travel) When these segments recover (or stabilize), they can drive earnings “surprise”.

-Soft Catalysts-

Defensive Rotation / Yield Preference (macro-driven)

Utilities and contracted-infrastructure names often benefit when investors rotate toward: lower earnings volatility, stable dividends,“bond proxy” equities. This isn’t a single event, but it can re-rate the stock even if the underlying operations don’t change much.

ESG and “Water Scarcity/Resilience” Thematic Flows

Water security is increasingly discussed as a climate-resilience issue. Even if Hong Kong’s total fresh-water demand is relatively stable, the importance of supply resilience can rise in investor attention, attracting ESG/thematic allocations to: water utilities, water infrastructure operators, wastewater and leakage-reduction ecosystems. 0270’s core identity as a major water-supply operator can benefit from that narrative.

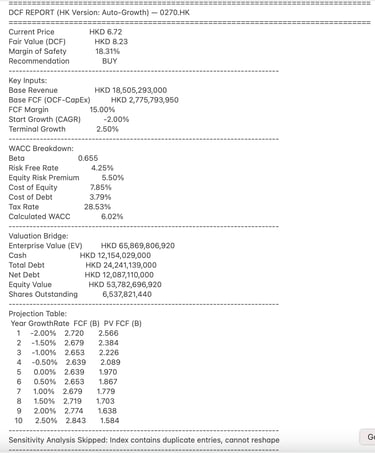

Valuation: DCF Model

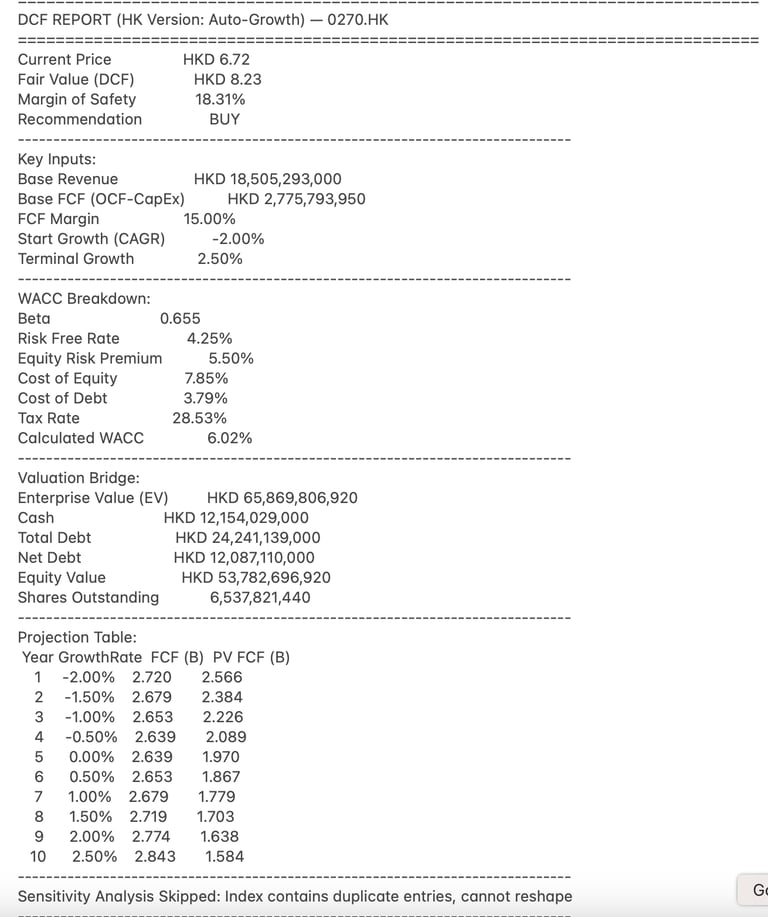

*Python Model Methodology & Disclaimer: The "Buy/Sell" rating indicates whether the current price offers a sufficient margin of safety (at least 15% discount) relative to the calculated Fair Value. This valuation is generated by an automated Discounted Cash Flow (DCF) model using public data from Yahoo Finance. For US stocks, the model assumes a "mean reversion" path where current growth rates gradually converge to a stable 2.5% economic average over the next decade. For HK stocks, the model applies a stricter "conservative decay" rule: while high growth slows down to the economic average, low historical growth remains flat rather than assuming automatic improvement. As this is a quantitative estimate relying on third-party data, it is provided for educational purposes only and does not constitute financial advice.

From the model, stock is modestly undervalued: with the share at HKD 6.72 versus a modeled fair value of HKD 8.23 (about 18% margin of safety, hence a BUY), the result is mainly driven by a normalized 15% FCF margin (base FCF ≈ HKD 2.78B on HKD 18.5B revenue), a growth path that improves from –2% toward +2.5% over 10 years (i.e., a recovery/mean-reversion assumption), and a low WACC of ~6.02% (supported by beta 0.655 and relatively cheap debt), with enterprise value (~HKD 65.9B) bridged to equity value (~HKD 53.8B) after net debt (~HKD 12.1B) and divided by ~6.54B shares.

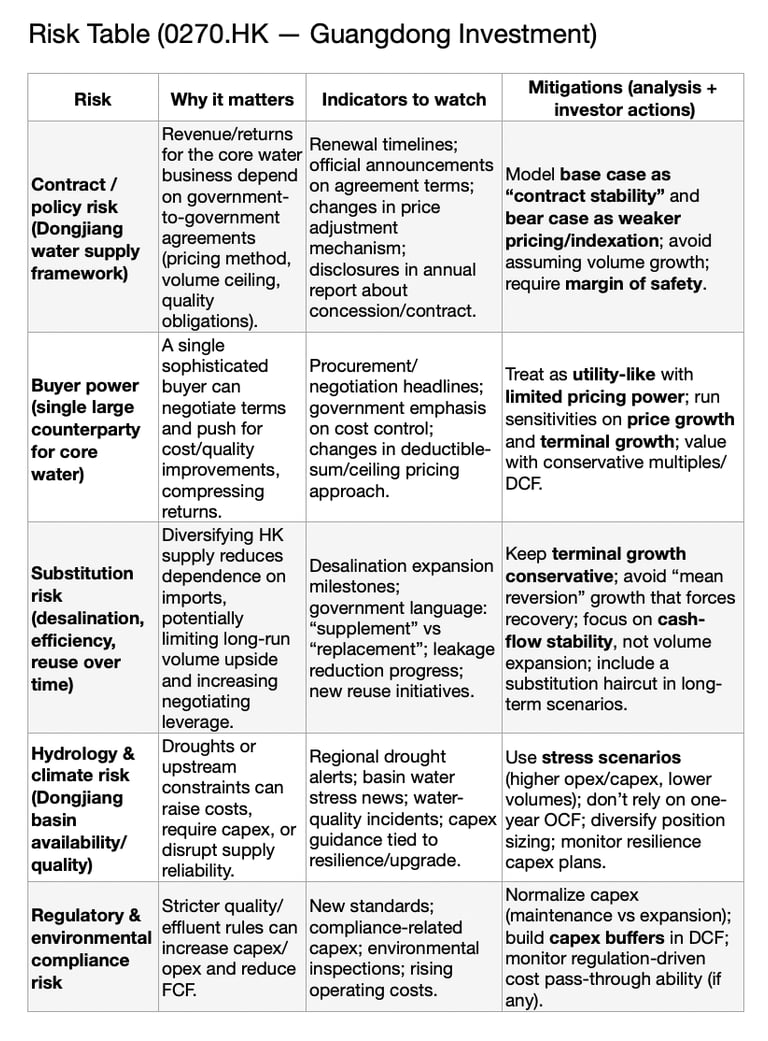

Risk Assessment & Mitigations

ESG Analysis

Environmental

Guangdong Investment Limited presents itself as an infrastructure-heavy group with ESG performance dominated by its Water Resources and Energy Projects segments, and its 2024 ESG report shows both significant environmental footprint and active mitigation. On the footprint side, the Group reported total greenhouse gas emissions of 3,273,835.78 tCO₂e in 2024, driven primarily by GDH Energy (Scope 1: 2,829,592.29 tCO₂e) while the Water Resources segment’s emissions are mainly electricity-related (Scope 2: 371,080.88 tCO₂e), reflecting the pump-and-treat energy intensity typical of water utilities; the Group also reports large-scale resource use (e.g., total water consumption 38,993,708.41 tonnes). On the mitigation and management side, the company describes a structured environmental management system aligned with ISO-style “three systems” (quality/environment/safety), states no major pollution incidents or major environmental penalties in 2024, and highlights tangible efficiency projects—e.g., upgrading units at Taiyuan Pumping Station increased efficiency from 68.5% to 70.5% with estimated annual savings of 1.6 million kWh, plus broader energy-saving upgrades across water pump houses and sewage plants. Importantly, GDI discloses forward-looking climate targets and governance: for Water Resources it targets a 36% reduction in carbon intensity by 2030 (vs FY2020) and 25% renewable energy proportion by 2030, and it also runs climate scenario analysis (low- vs high-emission scenarios) and mitigation measures such as emergency “three-control” planning (flood/drought/typhoon), water-quality monitoring systems, and annual All Risks Insurance coverage for property in response to physical climate risks.

Social

The social profile is anchored by “essential services + safety + people management,” with detailed operational and workforce KPIs. Operationally, GDI frames water supply quality and reliability as a core social responsibility: its Water Resources segment (which contributed 73.01% of Group revenue in 2024) reports that the overall pass rate of tap water reached 99.99%, and it emphasizes customer service infrastructure (e.g., hotline/online channels, training bases, monitoring centers) with reported customer satisfaction metrics (e.g., Water Holdings handled 620,000+ service matters and conducted 220,000+ return visits with 99.99% satisfaction). On safety and labor, the Group reports 0 work-related fatalities and 25 work-related injuries in 2024 (with 483.1 lost working days), and describes structured work-safety governance (safety committees, dual-prevention mechanism, emergency drills, and digital tools like “GDH Safety Management”). On talent and inclusion, it reports a total workforce of 10,988 employees (with 3,740 female employees), very high training coverage (~99.5%+ trained across genders and categories), and 327,363.32 total training hours (about 29.79 hours per employee). Community investment is also material: the Group reports 838,640 hours spent on volunteer activities in 2024, positioning community engagement as a significant pillar alongside product/service responsibility, privacy/information security controls, and supplier safety management requirements embedded into contracts and assessments.

Governance in the 2024 ESG report is described as formalized, compliance-oriented, and “top-down,” with explicit board oversight, committee structure, and controls that are typical for a large Hong Kong–listed, state-controlled enterprise. GDI states it has a robust ESG governance framework consisting of the Board, an ESG Committee, and an ESG Working Group, with board-level ESG work meetings held in March and August 2024 (including approval of the 2023 ESG report and revisions to multiple ESG policies), and it notes the 2024 ESG Report was approved by the Board on 24 March 2025. The company highlights a “Trinity+ Compliance Management Framework” and reports that GDI and key subsidiaries maintained ISO 37301:2021 compliance management system certification status through annual audits, supported by recurring compliance training and a “three lines of defence” risk-management model (business units; risk coordination; internal audit/supervision). On ethics, it reports zero concluded legal cases regarding corruption in 2024, requires employee integrity commitment letters, and describes whistleblowing channels (24/7 hotline/email), confidentiality protections, and anti-retaliation rules. Finally, it also emphasizes ESG data reliability by requiring ESG information disclosure undertaking letters from working-group members and deploying an ESG data management platform to digitize data collection—important context for investors who rely on reported KPIs across a diversified set of operating segments.

Governance

Credit Lens

A lender should underwrite Guangdong Investment as a predominantly infrastructure‑cash‑flow group with meaningful policy/contract exposure. The lending “comfort” comes from the visibility of the Hong Kong water pricing schedule (2024–2026 basic prices are explicitly disclosed) and the scale of the water segment’s contribution to group economics.

The main credit sensitivities are also unusually legible from the audited disclosure. First, interest‑rate sensitivity is not theoretical: the company discloses that 92.1% of borrowings are floating‑rate. Second, currency mismatch matters because borrowings are predominantly RMB while a meaningful portion of water revenue is HKD‑linked through the Hong Kong agreement. Third, conglomerate leakage can still appear through property valuation changes and weaker consumer segments, and the annual report explicitly quantifies investment property fair value movements and reports segment results that show which divisions are structurally more fragile.

From a covenant and structure perspective, a bank would normally aim for terms that keep the “water‑anchor” cash flows from being diluted by aggressive distributions or acquisitions during a downturn. This matters because the company’s audited highlights show a dividend payout ratio around 65%, which is friendly to equity but a real variable in liquidity planning for lenders.

On funding access, the public disclosures also show that the group uses committed bank facilities, including announcements in 2025 referring to a committed term loan facility in the principal amount of HK$2.25bn and a committed revolving loan facility in the principal amount of HK$1.75bn, both disclosed under HKEX Rule 13.18. Even without parsing every covenant, the existence and size of these facilities provide a useful signal that banks treat the name as bankable on a committed basis rather than purely transactional.

Transaction Banking Lens

The transaction banking opportunity here is fundamentally about running a large, multi‑segment, cross‑border operating group with fewer cash surprises and better control. Guangdong Investment’s audited segment table shows that almost all continuing‑operations revenue is generated in Mainland China, yet the group has large HKD‑linked contractual revenue components (Hong Kong water basic price is set in HK$) and a borrowings book that is mostly RMB and mostly floating. That combination naturally creates daily treasury decisions around currency positioning, liquidity buffers, and interest expense volatility.

In practical terms, a bank’s most “useful” TB work would likely center on cash visibility, cross‑border pooling, and automation. The group reports liquidity ratio and interest cover in its audited highlights, which suggests management monitors these metrics; TB tooling can help make those metrics more controllable in real time rather than only at reporting dates. Given the disclosed maturity ladder (with a meaningful within‑one‑year bucket) and high floating‑rate exposure, a bank can also build an integrated offering that connects operational cash management with policy‑based interest‑rate and FX execution, so the CFO’s world is not split between “treasury ops” and “markets” as separate silos.

Finally, because parts of the business are effectively infrastructure and public‑service adjacent, auditability and governance matter. The company explicitly discloses controlling shareholdings and related governance context; in such a structure, strong maker‑checker controls, entitlements management, and standardized reconciliation reduce operational risk and reduce the probability that governance perception becomes a valuation discount.