Use Desktop for Better Experience

Integrated Equity × Credit × Transaction Banking Report: Vantage Corp (VNTG)

Price reference date: December 24, 2025 (close: $0.90). Latest audited annual filing referenced: FY ended March 31, 2025 (Form 20‑F filed July 28, 2025).

FINANCIALSELECTED

Ryan Cheng

12/27/20258 min read

*Stocks and investments carry risks, including the loss of principal. The views expressed on this blog are solely the opinions of the author at the time of writing and are subject to change at any time without notice.

Company Overview

Vantage Corp (via its operating subsidiary Vantage Shipbrokers) is a specialized, tanker-focused brokerage platform headquartered in Singapore with a presence in Dubai. Founded in 2012, the firm has evolved from a pure-play freight brokerage into an integrated service provider covering Clean Petroleum Products (CPP), Dirty Petroleum Products (DPP)/Crude, Petrochemicals, and Biofuels/Vegetable Oils.

Core Business Function

Vantage operates not as a shipowner, but as a specialized broker and intermediary within the maritime industry. Acting as a "pivotal link" in the supply chain, the company connects shipowners with charterers—a diverse group that includes oil companies, commodity traders, and commercial managers. Vantage’s role extends beyond simple introductions; it actively identifies market opportunities, facilitates complex negotiations regarding charter terms, and provides ongoing support to ensure the successful execution of these agreements. By sitting in the middle of these transactions, Vantage helps both sides navigate the complexities of shipping logistics and contract management.

Strategic Support and Specialized Divisions

Vantage complements its spot chartering activities with services that address longer-term needs and operational efficiency. The Period Charters desk focuses on volatility and risk mitigation, offering clients optionality for trading over longer timeframes. For clients looking at fleet renewal or expansion, the Sales & Projects division handles long-term investment needs. Supporting all these deal-making desks is a dedicated Operations and Demurrage team, which ensures end-to-end execution and dispute resolution. Furthermore, the company distinguishes itself with a Research & Advisory arm that aims to "go beyond the data" to provide clients with actionable market insights.

Market Segmentation and Management Focus

According to the company’s audited 20-F filings, management formally segments its tanker services into five key divisions: Dirty Petroleum Products/Crude, Clean Petroleum Products, Petrochemicals, Biofuels and Vegetable Oils, and Projects. The "Projects" segment is particularly notable as it encompasses longer-term charters, including time charters spanning two to three years. This formal segmentation is significant because it signals how management views the business structure, likely influencing how they allocate capital, technology, and hiring resources across their various desks.

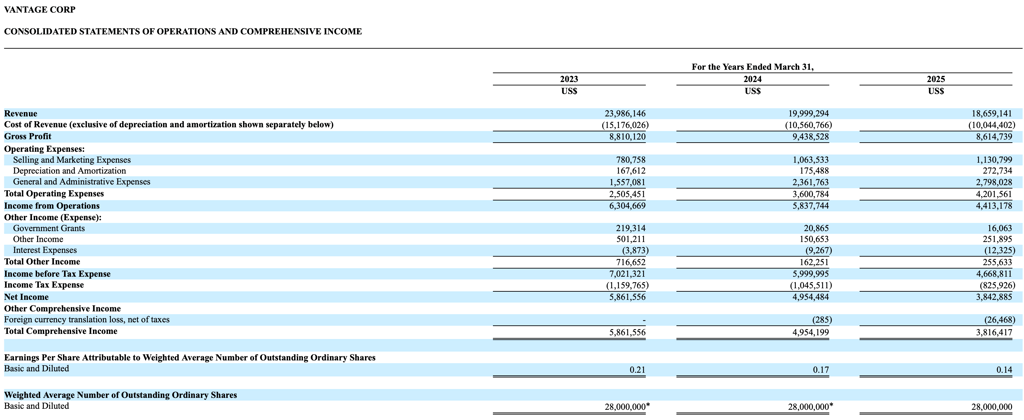

Financial Snapshot

source: sec.gov

On FY2025 numbers, gross margin is roughly 46% and net margin is roughly 21% (computed from audited revenue and net income), which is strong for a services business even after the downshift versus prior years.

Cash flow is the part of the story that complicates a simple “cheap P/E” interpretation. The 20‑F shows operating cash flow of $12.88M, $(0.17)M (FY2024), and $1.90M (FY2025), while year-end cash declined to $5.95M at March 31, 2025. Management attributes the reduction in cash mainly to dividends totaling $11.42M, and the balance sheet shows substantial dividend payable at year-end, with working capital reduced to $0.89M as of March 31, 2025. Since the IPO occurred after the FY2025 year-end, management also notes that IPO proceeds support near-term liquidity expectations.

At $0.90 on Dec 24, 2025 and with shares outstanding shown around 31.74M, the implied market capitalization is about $28.6M using simple price-times-shares arithmetic. The 20‑F describes an IPO priced at $4.00 per Class A share, with the underwriter over-allotment exercised for an additional 487,500 shares. That gap between IPO price and the later microcap trading level is part of what makes scenario thinking more useful than precise point estimates.

Governance is also central. Vantage has a dual-class structure where Class A carries one vote and Class B carries ten votes, and the 20‑F states that major shareholders owning all Class B shares control about 94.70% of the voting power. That does not automatically mean “bad,” but it does mean outside shareholders are underwriting the controlling holders’ capital allocation discipline for a long time.

Equity Valuation: multiples plus scenario bands

For a microcap with cyclical earnings and evolving share count, simple multiples can mislead unless you are explicit about your assumptions. Using the Dec 24, 2025 price of $0.90 and shares outstanding of 31.74M from StockAnalysis, market cap is roughly $28.6M. If you compare that to audited FY2025 net income of $3.84M, you get a rough P/E in the high single digits using “net income divided by current shares” as an EPS proxy, but it is important to remember that the audited EPS in the 20‑F uses a weighted-average share count presented around 28.0M, which differs from post-IPO shares and can distort screeners.

Because shipbroking earnings can move materially from year to year, the cleaner blog-friendly approach is to anchor on scenario earnings bands and apply conservative multiples to each band. Below is an illustrative table that uses the 31.74M share count and shows what various P/E multiples imply under down-, mid-, and up-cycle net income assumptions.

With the stock around $0.90 on the reference date, the market looks closer to pricing something like mid-cycle earnings at a modest multiple, without granting much optionality for acquisitions or data products until execution is clearer.

Stock & Governance Context

At $0.90 on Dec 24, 2025 and with shares outstanding shown around 31.74M, the implied market capitalization is about $28.6M using simple price-times-shares arithmetic. The 20‑F describes an IPO priced at $4.00 per Class A share, with the underwriter over-allotment exercised for an additional 487,500 shares. That gap between IPO price and the later microcap trading level is part of what makes scenario thinking more useful than precise point estimates.

Governance is also central. Vantage has a dual-class structure where Class A carries one vote and Class B carries ten votes, and the 20‑F states that major shareholders owning all Class B shares control about 94.70% of the voting power. That does not automatically mean “bad,” but it does mean outside shareholders are underwriting the controlling holders’ capital allocation discipline for a long time.

Equity Lens

The equity question here is whether Vantage remains a cyclical but profitable “relationship brokerage” or evolves into a broader platform where operations excellence, advisory, and eventually workflow/data tools increase client stickiness and perceived earnings durability. The company’s own positioning supports the narrative that it is trying to be more than a voice broker, and the audited financials show the model can produce real margins when conditions cooperate.

The main risks follow directly from the model. Earnings can swing with tanker market activity and fixture volumes; relationships can be portable when brokers move; and microcap liquidity can dominate fundamental valuation. The company itself flags penny-stock type risks in its filings and discloses the dual-class voting control that limits minority shareholder influence. On top of that, tanker-linked commercial flows typically raise compliance intensity for counterparties, which can create both friction and a need for strong controls.

Catalysts come down to evidence that the business is broadening in ways that the market will actually pay for. The company authorized a $1M share repurchase program through Dec 31, 2026, and it disclosed acquisition agreements to buy PJ Marine Singapore and majority stakes in affiliated entities for approximately $3.6M in cash across two installments. The related company announcement describes the acquisition target revenue and margin profile based on FY2024 results of those acquired companies, and indicates a closing timeline by end of Q1 2026. Separately, the most important operational catalyst is whether “digital/data/intelligence” becomes demonstrably productized, as signaled on the website and via the Opswiz reference in the 20‑F.

Credit Lens

A lender should view Vantage as a commission-driven, asset-light services firm where credit quality depends less on collateral and more on cash conversion discipline, working-capital management, and governance around distributions and acquisitions. The audited 20‑F shows meaningful dividend outflows and a large dividend payable that coincided with reduced year-end cash and reduced working capital as of March 31, 2025, which is exactly the kind of dynamic that a bank addresses with liquidity covenants and distribution restrictions (SEC 20‑F). The company also describes the IPO proceeds as supporting liquidity after year-end, but a bank typically does not lend on “we can raise equity” as a permanent protection; it lends on controls and recurring cash generation.

If structuring a revolving credit facility, the most practical protections are a minimum liquidity test, clear limits on dividends and buybacks while the facility is drawn, M&A approval rights given the company’s acquisition activity, and monthly reporting on cash and receivables aging. The operational emphasis the firm places on operations and demurrage support is relevant because it can reduce disputes that delay collections; from a credit standpoint, fewer disputes and cleaner documentation generally improve the predictability of cash receipts.

In short, Vantage has few tangible assets to pledge as collateral, and it likes to distribute cash to shareholders, which banks perceive as risky. Therefore, if a bank wants to lend money to it, it must strictly limit its spending and closely monitor its cash flow.

Transaction Banking Lens

Vantage’s service mix implies a treasury profile dominated by cross-border payments, multi-currency cash management, and high expectations for control and auditability, especially when flows are adjacent to tanker-linked commerce. A well-designed transaction banking setup can improve straight-through processing and reduce operational risk through better entitlements, maker-checker workflows, standardized remittance information, and more reliable reconciliation at the desk and client level. In practical terms, multi-currency operating accounts with virtual-account style sub-ledgers can reduce reconciliation friction; payment templates and approval matrices can reduce error rates; and a defined FX policy can reduce budget volatility if costs and revenues are mismatched across currencies.

The compliance overlay is not optional. Strong screening workflows, disciplined KYC refresh, and exception handling are not just “bank requirements”; they can make the company easier to bank and easier to do business with, which can support both resilience (credit) and client retention (equity).

In summary, Vantage is a company that handles complex cross-border financial transactions. To prevent chaos, it needs to manage its money using advanced banking tools such as virtual accounts and automated reconciliation, and it must conduct thorough anti-money laundering audits so that banks will trust it and the business can thrive in the long run.

What We Should Watch Next?

Vantage’s company website indicates two locations, specifically Singapore and Dubai. It also states that, as of 2023, the organization employed “over 40” people. The 20‑F provides an updated point-in-time figure, stating that the company had expanded to “over 59” professionals as of July 2025 in Singapore and Dubai, which suggests continued hiring and desk build-out.

The digital angle is not subtle in the company’s own narrative. The About Us page acknowledges competitive pressure and “digitalization” as a challenge, and then explicitly says the firm is embracing digital tools to enhance productivity and to launch into data and intelligence. The 20‑F adds a concrete datapoint by referencing an Enterprise Singapore grant to develop “Opswiz,” described as operations efficiency software tailored to the tanker market. If anything can change how investors think about a broker’s durability, it is evidence that workflow software and data products become real, used, and monetized rather than remaining aspirational.

The near-term narrative will likely be driven by whether announced acquisitions close on the stated timeline and whether they integrate cleanly into the platform, along with whether operating cash flow becomes more consistent relative to accounting earnings. In parallel, the most important strategic question is whether the company’s stated shift toward digitalization and data/intelligence produces tangible products or demonstrable productivity gains, because that is the clearest path to higher-quality, less purely cyclical perception over time.